Student Loan Interest: How It Works and Why It Costs More Than You Think

Published on: March 24, 2026

Introduction

If you have student loans — or are about to take them out — there is one number that will quietly shape your financial life for years: the interest rate. Most borrowers focus on the loan amount itself, but it is the interest that determines how much you actually pay back. And the answer is almost always more than people expect.

In the United States alone, outstanding student loan debt has surpassed $1.77 trillion, spread across roughly 43 million borrowers. The average graduate carries about $37,000 in education debt. But here is the part that catches people off guard: thanks to how interest accrues — especially during school and grace periods — many borrowers end up repaying $10,000 to $20,000 more than they originally borrowed.

This guide breaks down exactly how student loan interest works, why it adds up faster than you think, and what you can do to minimize the damage. We will also show you how to use our free Student Loan Calculator to model your exact situation and find the smartest repayment path.

How Student Loan Interest Works

Student loan interest is the cost a lender charges you for borrowing money. It is expressed as an annual percentage rate (APR) but calculated on a daily basis. This daily calculation is what makes student loan interest behave differently from what most people expect.

The Daily Interest Formula

Your lender uses a straightforward formula to determine how much interest accrues each day:

Daily Interest = (Loan Balance × Interest Rate) ÷ 365

For example, if you owe $30,000 at a 5.5% interest rate:

($30,000 × 0.055) ÷ 365 = $4.52 per day

That means $4.52 is being added to your balance every single day — weekends, holidays, and summer breaks included. Over a single month, that is roughly $137 in interest alone. Over a year, it is about $1,650. And remember — this is happening before you even start making payments.

When Does Interest Start?

This depends on the type of loan you have:

- Unsubsidized Federal Loans: Interest begins accruing the moment your loan is disbursed — while you are still in school, during your grace period, and during any deferment. The government does not cover this interest for you.

- Subsidized Federal Loans: The government pays the interest while you are enrolled at least half-time, during your grace period, and during eligible deferment periods. Interest only begins accruing on your dime once repayment starts.

- Private Student Loans: Interest almost always starts immediately upon disbursement, similar to unsubsidized loans. Terms vary by lender, but do not expect a free ride.

The critical takeaway: if you have unsubsidized or private loans, interest has been silently growing from the first day your tuition check was cashed.

Simple vs. Compound Interest: The Snowball Effect

Most federal student loans use simple interest — meaning interest is calculated only on the original principal balance, not on accumulated interest. This sounds manageable, and it is — as long as you are making payments.

The problem comes when unpaid interest gets capitalized.

What Is Interest Capitalization?

Capitalization happens when your unpaid accrued interest is added to your principal balance. Once that happens, you start paying interest on a larger balance — effectively turning simple interest into something that behaves like compound interest.

Capitalization typically occurs when:

- Your grace period ends and repayment begins

- A deferment or forbearance period ends

- You switch repayment plans

- You fail to recertify for an income-driven plan

A Real Example of Capitalization

Let us say you borrow $30,000 in unsubsidized loans at 5.5% and spend 4 years in school plus a 6-month grace period without making any payments:

Interest per year: $30,000 × 5.5% = $1,650

4.5 years of accrual: $1,650 × 4.5 = $7,425 in unpaid interest

New capitalized balance: $30,000 + $7,425 = $37,425

You have not spent a single dollar yet, and your loan has already grown by nearly 25%. From this point forward, your daily interest is calculated on $37,425 instead of $30,000 — costing you an extra $1.12 per day compared to the original balance. That compounds to roughly $409 more per year in interest alone.

This is why capitalization is often called a “silent balance inflator.” It is the single biggest reason people end up paying far more than they borrowed.

The Real Cost Over Time: What $30,000 Actually Costs You

Let us continue with our example. You borrowed $30,000, but after capitalization your balance is $37,425. Now you enter the standard 10-year repayment plan. Here is what the numbers actually look like:

| Scenario | Monthly Payment | Total Paid | Total Interest |

|---|---|---|---|

| Original $30,000 (no capitalization) | $326/mo | $39,074 | $9,074 |

| After capitalization ($37,425) | $406/mo | $48,743 | $18,743 |

Read that last number again: $18,743 in total interest on a $30,000 loan. That is more than 62% of your original loan amount added on top — and it is entirely because interest accrued silently for 4.5 years before repayment began.

Your monthly payment jumps by $80/month compared to the scenario with no capitalization. Over 10 years, those extra $80 payments add up to $9,669 in additional cost. That is money that could have gone to rent, retirement savings, or a down payment on a car.

What About Longer Repayment Terms?

Some borrowers choose extended repayment plans (20 or 25 years) to lower monthly payments. While this helps with cash flow, the interest cost becomes staggering:

- 10-year plan: ~$18,743 in total interest

- 20-year plan: ~$26,800 in total interest

- 25-year plan: ~$32,400 in total interest

On the 25-year plan, you would pay back more than double what you originally borrowed. The loan amount was $30,000, but the total out-of-pocket cost exceeds $62,000.

This is why understanding interest is not optional — it is the difference between paying $39K and $62K for the same education.

Federal vs. Private Student Loan Interest Rates

Not all student loans are created equal. The interest rate you receive depends heavily on whether your loan is federal or private, and this distinction affects everything from how much interest accrues to what repayment protections you have.

Federal Student Loan Rates

Federal loan rates are set by Congress each year and remain fixed for the life of the loan. For the 2024-2025 academic year, the rates are:

- Direct Subsidized & Unsubsidized (Undergraduate): 6.53% fixed

- Direct Unsubsidized (Graduate): 8.08% fixed

- Direct PLUS (Parents & Grad Students): 9.08% fixed

Federal loans come with borrower protections like income-driven repayment plans, deferment options, and potential loan forgiveness programs (such as Public Service Loan Forgiveness). These protections make federal loans the safer choice for most students.

Private Student Loan Rates

Private lenders (banks, credit unions, online lenders) set their own rates based on your credit score, income, and cosigner. Rates can be:

- Fixed: Typically 4% to 15%, depending on creditworthiness

- Variable: May start lower (3% to 12%) but can increase over time as market rates change

While private loans can offer lower rates for borrowers with excellent credit, they come with fewer protections. There is no income-driven repayment, limited deferment options, and no forgiveness programs. If you are comparing options, always exhaust federal loan eligibility before turning to private lenders.

7 Strategies to Reduce Your Student Loan Interest

The good news: you are not powerless against student loan interest. Here are proven strategies that can save you thousands over the life of your loan — some you can start today:

1. Make Interest-Only Payments While in School

This is the single most impactful thing you can do. If you have unsubsidized loans, paying just the monthly interest while you are enrolled prevents capitalization entirely. In our $30,000 example, that means paying $137/month during school — which saves you $9,669 over the life of the loan.

Even if you cannot cover the full interest amount, paying something each month reduces the balance that gets capitalized.

2. Pay More Than the Minimum

Once you are in repayment, even small extra payments make a massive difference. Adding just $50/month to a $37,425 loan at 5.5% over 10 years saves you roughly $2,800 in interest and pays off the loan 14 months early.

Important: Tell your loan servicer to apply extra payments to the principal, not future payments. By default, some servicers will advance your due date instead of reducing your balance — which does not save you interest.

3. Use the Avalanche Method

If you have multiple loans, the avalanche method targets the loan with the highest interest rate first while making minimum payments on the rest. This mathematically minimizes total interest paid. It requires discipline, but the savings are real.

Alternatively, the snowball method targets the smallest balance first for psychological momentum. It costs a bit more in interest, but the quick wins can keep you motivated.

4. Set Up Autopay for the Rate Discount

Most federal and private loan servicers offer a 0.25% interest rate reduction when you enroll in automatic payments. On a $37,425 balance, that tiny reduction saves you about $500 over a 10-year term. It takes 5 minutes to set up and costs you nothing.

5. Consider Refinancing (Carefully)

If you have strong credit and stable income after graduation, refinancing can lower your interest rate significantly — sometimes by 2-3 percentage points. On a $37,425 balance, dropping from 5.5% to 3.5% saves roughly $4,200 over 10 years.

Warning: Refinancing federal loans into a private loan means losing access to income-driven repayment, deferment, forbearance, and forgiveness programs. Only refinance federal loans if you are confident you will not need those safety nets.

6. Explore Forgiveness Programs

If you work in public service, education, or certain non-profit roles, you may qualify for Public Service Loan Forgiveness (PSLF). After 120 qualifying payments (10 years), the remaining balance is forgiven — tax-free. Income-driven repayment plans like SAVE, PAYE, and IBR also offer forgiveness after 20-25 years, though the forgiven amount may be taxable.

7. Claim the Student Loan Interest Deduction

You may be able to deduct up to $2,500 of student loan interest paid per year on your federal tax return (even if you do not itemize). This effectively reduces your interest cost. Income limits apply, but most recent graduates qualify. Check IRS Form 1098-E or consult a tax professional.

See Your Numbers: Use the Student Loan Calculator

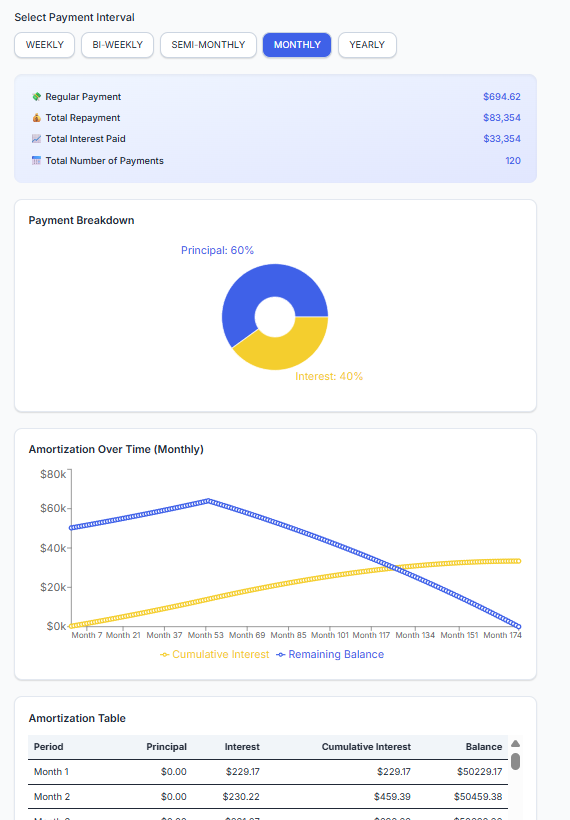

Everything we have discussed — daily interest accrual, capitalization, the cost of different repayment terms — comes alive when you plug in your own numbers. Our free Student Loan Calculator is built specifically for education loans and accounts for factors that generic calculators miss.

What You Can Calculate

Enter your loan details and instantly see:

- Monthly Payment: Your exact payment amount based on loan balance, rate, and term

- Total Interest Paid: The full cost of borrowing over the entire repayment period

- Total Repayment Amount: Principal plus all interest combined

- In-School Interest Accrual: Toggle whether interest accumulates during your school years — and see exactly how much capitalization adds to your balance

- Grace Period Modeling: Set your grace period length and watch how those extra months of accrual affect your total cost

- Amortization Schedule: A month-by-month breakdown showing how each payment is split between principal and interest

- Visual Charts: Pie chart of principal vs. interest, plus a graph showing your balance declining over time

Try These Scenarios

Use the calculator to compare these common situations and see the difference for yourself:

- With vs. without in-school interest accrual — Toggle the checkbox to see how paying interest during school changes your total cost

- 10-year vs. 20-year repayment term — See how stretching payments saves monthly but costs thousands more overall

- Different interest rates — Compare your federal rate against a potential refinancing rate

- Shorter grace period — See how starting repayment sooner can reduce capitalized interest

Conclusion

Student loan interest is not just a percentage on a piece of paper — it is a daily, compounding force that can add tens of thousands of dollars to what you owe. The difference between a borrower who understands interest and one who does not can be $10,000 or more over the life of the same loan.

The key takeaways are simple: know when your interest starts accruing, understand what capitalization does to your balance, and take action early. Even small steps — paying interest during school, adding $50/month to your minimum, or setting up autopay — compound in your favor the same way interest compounds against you.

Use our Student Loan Calculator to run the numbers for your specific situation. See exactly what you will pay, explore different scenarios, and make a repayment plan that fits your life. Knowledge is the best weapon against student loan interest — and now you have it.

Need to calculate other financial scenarios? Explore our full suite of tools:

- Student Loan Calculator — Model repayment with in-school accrual, grace periods, and amortization schedules.

- Mortgage Calculator — Estimate home loan payments with PITI breakdowns.

- Auto Loan Calculator — Compare car financing options and total loan cost.

- Scientific Calculator — A fast, free calculator for any quick math you need.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Interest rates and repayment figures are illustrative examples. Always consult a licensed financial advisor for personalized guidance regarding your student loans.